कमाल काढण्यायोग्य मूल्य (MEV)

कमाल काढण्यायोग्य मूल्य (MEV) म्हणजे ब्लॉक उत्पादनातून मानक ब्लॉक बक्षीस आणि गॅस शुल्काव्यतिरिक्त, ब्लॉकमधील व्यवहारांचा समावेश करून, वगळून आणि त्यांचा क्रम बदलून काढता येणारे जास्तीत जास्त मूल्य होय.

कमाल काढण्यायोग्य मूल्य

कमाल काढण्यायोग्य मूल्य प्रथम प्रूफ-ऑफ-वर्क च्या संदर्भात लागू केले गेले आणि सुरुवातीला त्याला "मायनर काढण्यायोग्य मूल्य" असे म्हटले गेले. याचे कारण असे की प्रूफ-ऑफ-वर्क मध्ये, मायनर व्यवहारांचा समावेश, वगळणे आणि क्रमवारी नियंत्रित करतात. तथापि, द मर्ज द्वारे प्रूफ-ऑफ-स्टेक मध्ये संक्रमण झाल्यापासून प्रमाणक या भूमिकांसाठी जबाबदार आहेत आणि खनन आता इथेरियम प्रोटोकॉलचा भाग नाही. तरीही मूल्य काढण्याच्या पद्धती अजूनही अस्तित्वात आहेत, त्यामुळे आता त्याऐवजी "कमाल काढण्यायोग्य मूल्य" हा शब्द वापरला जातो.

पूर्वअटी

तुम्हाला व्यवहार, ब्लॉक, प्रूफ-ऑफ-स्टेक आणि गॅस ची माहिती असल्याची खात्री करा. विकेंद्रित ॲप्लिकेशन (dapp) आणि विकेंद्रित वित्त (DeFi) ची माहिती असणे देखील उपयुक्त आहे.

MEV काढणे

सैद्धांतिकदृष्ट्या MEV पूर्णपणे प्रमाणकांना मिळते कारण ते एकमेव पक्ष आहेत जे फायदेशीर MEV संधीच्या अंमलबजावणीची हमी देऊ शकतात. प्रत्यक्षात मात्र, MEV चा मोठा भाग "शोधक" (searchers) म्हणून ओळखल्या जाणाऱ्या स्वतंत्र नेटवर्क सहभागींद्वारे काढला जातो. शोधक फायदेशीर MEV संधी शोधण्यासाठी ब्लॉकचेन डेटावर जटिल अल्गोरिदम चालवतात आणि ते फायदेशीर व्यवहार नेटवर्कवर स्वयंचलितपणे सबमिट करण्यासाठी त्यांच्याकडे बॉट्स असतात.

प्रमाणकांना तरीही संपूर्ण MEV रकमेचा काही भाग मिळतो कारण शोधक त्यांच्या फायदेशीर व्यवहारांचा ब्लॉकमध्ये समावेश होण्याची शक्यता वाढवण्यासाठी जास्त गॅस शुल्क (जे प्रमाणकाला जाते) देण्यास तयार असतात. शोधक आर्थिकदृष्ट्या तर्कसंगत आहेत असे गृहीत धरल्यास, शोधक जे गॅस शुल्क देण्यास तयार असेल ती रक्कम शोधकाच्या MEV च्या 100% पर्यंत असेल (कारण जर गॅस शुल्क जास्त असेल तर शोधकाचे नुकसान होईल).

यासह, DEX आर्बिट्रेज सारख्या काही अत्यंत स्पर्धात्मक MEV संधींसाठी, शोधकांना त्यांच्या एकूण MEV महसुलाच्या 90% किंवा त्याहून अधिक रक्कम गॅस शुल्क म्हणून प्रमाणकाला द्यावी लागू शकते कारण अनेक लोकांना तोच फायदेशीर आर्बिट्रेज व्यापार चालवायचा असतो. याचे कारण असे की त्यांचा आर्बिट्रेज व्यवहार चालेल याची हमी देण्याचा एकमेव मार्ग म्हणजे त्यांनी सर्वाधिक गॅसच्या किंमतीसह व्यवहार सबमिट करणे.

गॅस गोल्फिंग

या गतिशीलतेमुळे "गॅस गोल्फिंग" मध्ये पारंगत असणे — व्यवहारांचे प्रोग्रामिंग करणे जेणेकरून ते कमीतकमी गॅस वापरतील — हा एक स्पर्धात्मक फायदा बनला आहे, कारण यामुळे शोधकांना त्यांचे एकूण गॅस शुल्क स्थिर ठेवून जास्त गॅसची किंमत सेट करण्याची परवानगी मिळते (कारण गॅस शुल्क = गॅसची किंमत * वापरलेला गॅस).

काही सुप्रसिद्ध गॅस गोल्फ तंत्रांमध्ये हे समाविष्ट आहे: शून्यांच्या लांब स्ट्रिंगने सुरू होणारे पत्ते वापरणे (उदा., 0x0000000000C521824EaFf97Eac7B73B084ef9306 (नवीन टॅबमध्ये उघडते)) कारण त्यांना संचयित करण्यासाठी कमी जागा (आणि म्हणून गॅस) लागते; आणि करारांमध्ये लहान ERC-20 टोकन शिल्लक ठेवणे, कारण स्टोरेज स्लॉट अद्यतनित करण्यापेक्षा स्टोरेज स्लॉट सुरू करण्यासाठी (शिल्लक 0 असल्यास) जास्त गॅस लागतो. गॅसचा वापर कमी करण्यासाठी अधिक तंत्रे शोधणे हे शोधकांमध्ये संशोधनाचे एक सक्रिय क्षेत्र आहे.

सामान्यीकृत फ्रंटरनर

फायदेशीर MEV संधी शोधण्यासाठी जटिल अल्गोरिदम प्रोग्राम करण्याऐवजी, काही शोधक सामान्यीकृत फ्रंटरनर चालवतात. सामान्यीकृत फ्रंटरनर हे बॉट्स आहेत जे फायदेशीर व्यवहार शोधण्यासाठी मेमपूल पाहतात. फ्रंटरनर संभाव्य फायदेशीर व्यवहाराचा कोड कॉपी करेल, पत्ते फ्रंटरनरच्या पत्त्याने बदलेल आणि सुधारित व्यवहारामुळे फ्रंटरनरच्या पत्त्यावर नफा होतो की नाही हे पुन्हा तपासण्यासाठी व्यवहार स्थानिक पातळीवर चालवेल. जर व्यवहार खरोखरच फायदेशीर असेल, तर फ्रंटरनर बदललेल्या पत्त्यासह आणि जास्त गॅसच्या किंमतीसह सुधारित व्यवहार सबमिट करेल, मूळ व्यवहाराला "फ्रंटरन" करेल आणि मूळ शोधकाचे MEV मिळवेल.

Flashbots

Flashbots हा एक स्वतंत्र प्रकल्प आहे जो अंमलबजावणी क्लायंटला अशा सेवेसह विस्तारित करतो जी शोधकांना सार्वजनिक मेमपूलमध्ये उघड न करता प्रमाणकांना MEV व्यवहार सबमिट करण्याची परवानगी देते. हे सामान्यीकृत फ्रंटरनर्सद्वारे व्यवहारांना फ्रंटरन होण्यापासून प्रतिबंधित करते.

MEV उदाहरणे

ब्लॉकचेनवर MEV काही मार्गांनी उदयास येते.

DEX आर्बिट्रेज

(DEX) आर्बिट्रेज ही सर्वात सोपी आणि सुप्रसिद्ध MEV संधी आहे. परिणामी, ती सर्वात स्पर्धात्मक देखील आहे.

हे असे कार्य करते: जर दोन DEX एकाच टोकनला दोन वेगवेगळ्या किंमतींवर ऑफर करत असतील, तर कोणीतरी कमी किंमतीच्या DEX वर टोकन खरेदी करू शकतो आणि एकाच, अणू (atomic) व्यवहारामध्ये जास्त किंमतीच्या DEX वर विकू शकतो. ब्लॉकचेनच्या यंत्रणेमुळे, हे खरे, जोखीममुक्त आर्बिट्रेज आहे.

येथे एका फायदेशीर आर्बिट्रेज व्यवहाराचे उदाहरण आहे (नवीन टॅबमध्ये उघडते) जिथे एका शोधकाने युनिस्वॅप विरुद्ध Sushiswap वर ETH/DAI जोडीच्या वेगवेगळ्या किंमतींचा फायदा घेऊन 1,000 ETH चे 1,045 ETH मध्ये रूपांतर केले.

रोखीकरण

कर्ज देण्याच्या प्रोटोकॉलचे रोखीकरण ही आणखी एक सुप्रसिद्ध MEV संधी सादर करते.

मेकर आणि आवे सारख्या कर्ज देण्याच्या प्रोटोकॉलसाठी वापरकर्त्यांना काही तारण (उदा., ETH) जमा करणे आवश्यक असते. हे जमा केलेले तारण नंतर इतर वापरकर्त्यांना कर्ज देण्यासाठी वापरले जाते.

वापरकर्ते नंतर त्यांच्या गरजेनुसार (उदा., जर तुम्हाला मेकरडाओ प्रशासन प्रस्तावामध्ये मत द्यायचे असेल तर तुम्ही MKR कर्ज घेऊ शकता) त्यांच्या जमा केलेल्या तारणाच्या विशिष्ट टक्केवारीपर्यंत इतरांकडून मालमत्ता आणि टोकन कर्ज घेऊ शकतात. उदाहरणार्थ, जर कर्ज घेण्याची रक्कम जास्तीत जास्त 30% असेल, तर जो वापरकर्ता प्रोटोकॉलमध्ये 100 DAI जमा करतो तो दुसऱ्या मालमत्तेचे 30 DAI मूल्यापर्यंत कर्ज घेऊ शकतो. प्रोटोकॉल अचूक कर्ज घेण्याच्या क्षमतेची टक्केवारी निर्धारित करतो.

कर्ज घेणाऱ्याच्या तारणाचे मूल्य जसे बदलते, तशीच त्यांची कर्ज घेण्याची क्षमता देखील बदलते. जर, बाजारातील चढउतारांमुळे, कर्ज घेतलेल्या मालमत्तेचे मूल्य त्यांच्या तारणाच्या मूल्याच्या समजा 30% पेक्षा जास्त झाले (पुन्हा, अचूक टक्केवारी प्रोटोकॉलद्वारे निर्धारित केली जाते), तर प्रोटोकॉल सामान्यतः कोणालाही तारणाचे रोखीकरण करण्याची परवानगी देतो, कर्ज देणाऱ्यांना त्वरित पैसे देतो (हे पारंपारिक वित्तामध्ये मार्जिन कॉल्स (नवीन टॅबमध्ये उघडते) कसे कार्य करतात यासारखेच आहे). रोखीकरण झाल्यास, कर्ज घेणाऱ्याला सहसा मोठी रोखीकरण फी भरावी लागते, ज्यातील काही भाग लिक्विडेटरला जातो — आणि इथेच MEV संधी येते.

कोणते कर्ज घेणारे रोखीकरणास पात्र आहेत हे निर्धारित करण्यासाठी आणि रोखीकरण व्यवहार सबमिट करणारे पहिले होण्यासाठी आणि स्वतःसाठी रोखीकरण फी गोळा करण्यासाठी शोधक शक्य तितक्या वेगाने ब्लॉकचेन डेटा पार्स करण्यासाठी स्पर्धा करतात.

सँडविच ट्रेडिंग

सँडविच ट्रेडिंग ही MEV काढण्याची आणखी एक सामान्य पद्धत आहे.

सँडविच करण्यासाठी, शोधक मोठ्या DEX व्यापारांसाठी मेमपूल पाहतो. उदाहरणार्थ, समजा कोणाला युनिस्वॅप वर DAI सह 10,000 UNI खरेदी करायचे आहेत. या प्रमाणाच्या व्यापाराचा UNI/DAI जोडीवर अर्थपूर्ण परिणाम होईल, ज्यामुळे DAI च्या तुलनेत UNI ची किंमत लक्षणीयरीत्या वाढण्याची शक्यता आहे.

शोधक UNI/DAI जोडीवर या मोठ्या व्यापाराच्या अंदाजे किंमतीच्या परिणामाची गणना करू शकतो आणि मोठ्या व्यापाराच्या लगेच आधी एक इष्टतम खरेदी ऑर्डर कार्यान्वित करू शकतो, UNI स्वस्तात खरेदी करू शकतो, नंतर मोठ्या व्यापाराच्या लगेच नंतर विक्री ऑर्डर कार्यान्वित करू शकतो, मोठ्या ऑर्डरमुळे वाढलेल्या किंमतीला ते विकू शकतो.

सँडविचिंग, तथापि, अधिक धोकादायक आहे कारण ते अणू (atomic) नाही (वर वर्णन केल्याप्रमाणे DEX आर्बिट्रेजच्या विपरीत) आणि साल्मोनेला हल्ल्यास (नवीन टॅबमध्ये उघडते) बळी पडण्याची शक्यता असते.

NFT MEV

NFT क्षेत्रात MEV ही एक उदयोन्मुख घटना आहे आणि ती नेहमीच फायदेशीर नसते.

तथापि, NFT व्यवहार इतर सर्व इथेरियम व्यवहारांद्वारे सामायिक केलेल्या त्याच ब्लॉकचेनवर होत असल्याने, शोधक NFT मार्केटमध्ये पारंपारिक MEV संधींमध्ये वापरल्या जाणाऱ्या तंत्रांसारखीच तंत्रे वापरू शकतात.

उदाहरणार्थ, जर एखादा लोकप्रिय NFT ड्रॉप असेल आणि शोधकाला एखादा विशिष्ट NFT किंवा NFT चा संच हवा असेल, तर ते अशा प्रकारे व्यवहाराचे प्रोग्रामिंग करू शकतात की ते NFT खरेदी करण्यासाठी रांगेत पहिले असतील, किंवा ते एकाच व्यवहारात NFT चा संपूर्ण संच खरेदी करू शकतात. किंवा जर एखादा NFT चुकून कमी किंमतीत सूचीबद्ध केला असेल (नवीन टॅबमध्ये उघडते), तर शोधक इतर खरेदीदारांना फ्रंटरन करू शकतो आणि तो स्वस्तात मिळवू शकतो.

NFT MEV चे एक प्रमुख उदाहरण तेव्हा घडले जेव्हा एका शोधकाने तळाच्या किंमतीला प्रत्येक Cryptopunk खरेदी करण्यासाठी (नवीन टॅबमध्ये उघडते) $7 दशलक्ष खर्च केले. एका ब्लॉकचेन संशोधकाने ट्विटर् वर स्पष्ट केले (नवीन टॅबमध्ये उघडते) की खरेदीदाराने त्यांची खरेदी गुप्त ठेवण्यासाठी MEV प्रदात्यासोबत कसे काम केले.

द लाँग टेल

DEX आर्बिट्रेज, रोखीकरण आणि सँडविच ट्रेडिंग या सर्व अतिशय सुप्रसिद्ध MEV संधी आहेत आणि नवीन शोधकांसाठी त्या फायदेशीर असण्याची शक्यता कमी आहे. तथापि, कमी ज्ञात MEV संधींची एक लांब रांग (long tail) आहे (NFT MEV ही अशीच एक संधी आहे).

जे शोधक नुकतीच सुरुवात करत आहेत त्यांना या लांब रांगेत MEV शोधून अधिक यश मिळू शकेल. Flashbot चे MEV जॉब बोर्ड (नवीन टॅबमध्ये उघडते) काही उदयोन्मुख संधी सूचीबद्ध करते.

MEV चे परिणाम

MEV पूर्णपणे वाईट नाही — इथेरियमवरील MEV चे सकारात्मक आणि नकारात्मक दोन्ही परिणाम आहेत.

चांगले

अनेक विकेंद्रित वित्त (DeFi) प्रकल्प त्यांच्या प्रोटोकॉलची उपयुक्तता आणि स्थिरता सुनिश्चित करण्यासाठी आर्थिकदृष्ट्या तर्कसंगत घटकांवर अवलंबून असतात. उदाहरणार्थ, DEX आर्बिट्रेज हे सुनिश्चित करते की वापरकर्त्यांना त्यांच्या टोकनसाठी सर्वोत्तम, सर्वात योग्य किंमती मिळतील आणि जेव्हा कर्ज घेणारे तारण प्रमाणाखाली येतात तेव्हा कर्ज देणाऱ्यांना त्यांचे पैसे परत मिळतील याची खात्री करण्यासाठी कर्ज देण्याचे प्रोटोकॉल जलद रोखीकरणावर अवलंबून असतात.

आर्थिक अकार्यक्षमता शोधणारे आणि दुरुस्त करणारे आणि प्रोटोकॉलच्या आर्थिक प्रोत्साहनांचा फायदा घेणारे तर्कसंगत शोधक नसल्यास, विकेंद्रित वित्त (DeFi) प्रोटोकॉल आणि विकेंद्रित ॲप्लिकेशन (dapp) सर्वसाधारणपणे आजच्याइतके मजबूत नसतील.

वाईट

ॲप्लिकेशन स्तरावर, सँडविच ट्रेडिंगसारख्या MEV च्या काही प्रकारांमुळे वापरकर्त्यांसाठी स्पष्टपणे वाईट अनुभव येतो. सँडविच झालेल्या वापरकर्त्यांना वाढीव स्लिपेज आणि त्यांच्या व्यापारांवर वाईट अंमलबजावणीचा सामना करावा लागतो.

नेटवर्क स्तरावर, सामान्यीकृत फ्रंटरनर्स आणि ते अनेकदा ज्या गॅस-किंमत लिलावांमध्ये गुंततात (जेव्हा दोन किंवा अधिक फ्रंटरनर्स त्यांच्या स्वतःच्या व्यवहारांची गॅसची किंमत उत्तरोत्तर वाढवून पुढील ब्लॉकमध्ये त्यांच्या व्यवहाराचा समावेश करण्यासाठी स्पर्धा करतात) त्यामुळे नेटवर्कची गर्दी होते आणि नियमित व्यवहार चालवण्याचा प्रयत्न करणाऱ्या इतर सर्वांसाठी गॅसच्या किंमती जास्त होतात.

ब्लॉकच्या आत जे घडत आहे त्यापलीकडे, MEV चे ब्लॉकच्या दरम्यान हानिकारक परिणाम होऊ शकतात. जर ब्लॉकमध्ये उपलब्ध MEV मानक ब्लॉक बक्षीसापेक्षा लक्षणीयरीत्या जास्त असेल, तर प्रमाणकांना ब्लॉक रि-ऑर्ग करण्यासाठी आणि स्वतःसाठी MEV कॅप्चर करण्यासाठी प्रोत्साहन दिले जाऊ शकते, ज्यामुळे ब्लॉकचेन पुनर्रचना आणि एकमत अस्थिरता निर्माण होते.

ब्लॉकचेन पुनर्रचनेची ही शक्यता यापूर्वी बिटकॉइन ब्लॉकचेनवर शोधली गेली आहे (नवीन टॅबमध्ये उघडते). जसजसे बिटकॉइनचे ब्लॉक बक्षीस निम्मे होते आणि व्यवहार शुल्क ब्लॉक बक्षीसाचा अधिकाधिक मोठा भाग बनवते, तसतशी अशी परिस्थिती उद्भवते जिथे मायनर्ससाठी पुढील ब्लॉकचे बक्षीस सोडून देणे आणि त्याऐवजी जास्त शुल्कासह मागील ब्लॉक पुन्हा माइन करणे आर्थिकदृष्ट्या तर्कसंगत बनते. MEV च्या वाढीसह, इथेरियममध्येही अशीच परिस्थिती उद्भवू शकते, ज्यामुळे ब्लॉकचेनच्या अखंडतेला धोका निर्माण होऊ शकतो.

MEV ची स्थिती

2021 च्या सुरुवातीला MEV काढण्याचे प्रमाण खूप वाढले, परिणामी वर्षाच्या पहिल्या काही महिन्यांत गॅसच्या किंमती अत्यंत जास्त होत्या. Flashbots च्या MEV रिलेच्या उदयामुळे सामान्यीकृत फ्रंटरनर्सची प्रभावीता कमी झाली आहे आणि गॅस किंमतीचे लिलाव साखळीबाह्य नेले आहेत, ज्यामुळे सामान्य वापरकर्त्यांसाठी गॅसच्या किंमती कमी झाल्या आहेत.

जरी अनेक शोधक अजूनही MEV मधून चांगले पैसे कमवत असले तरी, जसजशा संधी अधिक सुप्रसिद्ध होतात आणि अधिकाधिक शोधक एकाच संधीसाठी स्पर्धा करतात, तसतसे प्रमाणक अधिकाधिक एकूण MEV महसूल कॅप्चर करतील (कारण वर वर्णन केल्याप्रमाणेच गॅस लिलाव Flashbots मध्ये देखील होतात, जरी खाजगीरित्या, आणि प्रमाणक परिणामी गॅस महसूल कॅप्चर करतील). MEV हे केवळ इथेरियमपुरते मर्यादित नाही आणि इथेरियमवरील संधी अधिक स्पर्धात्मक होत असल्याने, शोधक बायनान्स् स्मार्ट चेन सारख्या पर्यायी ब्लॉकचेनकडे वळत आहेत, जिथे इथेरियमसारख्याच MEV संधी कमी स्पर्धेसह अस्तित्वात आहेत.

दुसरीकडे, प्रूफ-ऑफ-वर्क मधून प्रूफ-ऑफ-स्टेक मध्ये संक्रमण आणि रोलअप्स वापरून इथेरियम स्केल करण्याचा चालू असलेला प्रयत्न हे सर्व MEV चे स्वरूप अशा प्रकारे बदलतात जे अद्याप काहीसे अस्पष्ट आहेत. प्रूफ-ऑफ-वर्क मधील संभाव्य मॉडेलच्या तुलनेत थोडे आधीच ज्ञात असलेले हमी दिलेले ब्लॉक-प्रस्तावक असण्याने MEV काढण्याची गतिशीलता कशी बदलते किंवा जेव्हा सिंगल सिक्रेट लीडर इलेक्शन (नवीन टॅबमध्ये उघडते) आणि वितरित व्हॅलिडेटर तंत्रज्ञान (DVT) लागू केले जाईल तेव्हा यात कसा व्यत्यय येईल हे अद्याप चांगले ज्ञात नाही. त्याचप्रमाणे, जेव्हा बहुतेक वापरकर्ता क्रियाकलाप इथेरियमवरून त्याच्या स्तर 2 (L2) रोलअप्स आणि शार्ड्सवर पोर्ट केले जातात तेव्हा कोणत्या MEV संधी अस्तित्वात असतात हे पाहणे बाकी आहे.

इथेरियम प्रूफ-ऑफ-स्टेक (PoS) मध्ये MEV

स्पष्ट केल्याप्रमाणे, MEV चे एकूण वापरकर्ता अनुभव आणि सहमती स्तर सुरक्षिततेवर नकारात्मक परिणाम होतात. परंतु इथेरियमचे प्रूफ-ऑफ-स्टेक एकमतामध्ये संक्रमण ("द मर्ज" असे नाव दिलेले) संभाव्यतः नवीन MEV-संबंधित धोके आणते:

प्रमाणक केंद्रीकरण

मर्ज-नंतरच्या इथेरियममध्ये, प्रमाणक (32 ETH ची सुरक्षा ठेव ठेवून) बीकन साखळी मध्ये जोडलेल्या ब्लॉकच्या वैधतेवर एकमत करतात. 32 ETH अनेकांच्या आवाक्याबाहेर असू शकत असल्याने, स्टेकिंग पूलमध्ये सामील होणे हा अधिक व्यवहार्य पर्याय असू शकतो. तरीही, सोलो स्टेकर चे निरोगी वितरण आदर्श आहे, कारण ते प्रमाणकांचे केंद्रीकरण कमी करते आणि इथेरियमची सुरक्षा सुधारते.

तथापि, MEV काढणे प्रमाणक केंद्रीकरणाला गती देण्यास सक्षम असल्याचे मानले जाते. हे अंशतः कारण आहे की, मायनर्सच्या तुलनेत प्रमाणक ब्लॉक प्रस्तावित करण्यासाठी कमी कमावतात, द मर्ज पासून MEV काढण्याने प्रमाणकांच्या कमाईवर (नवीन टॅबमध्ये उघडते) खूप प्रभाव टाकला आहे.

मोठ्या स्टेकिंग पूलकडे MEV संधी कॅप्चर करण्यासाठी आवश्यक ऑप्टिमायझेशनमध्ये गुंतवणूक करण्यासाठी अधिक संसाधने असण्याची शक्यता आहे. हे पूल जितके जास्त MEV काढतील, तितकी त्यांच्याकडे त्यांची MEV-काढण्याची क्षमता सुधारण्यासाठी (आणि एकूण महसूल वाढवण्यासाठी) अधिक संसाधने असतील, ज्यामुळे मूलत: प्रमाणाचे अर्थशास्त्र (economies of scale) (नवीन टॅबमध्ये उघडते) निर्माण होईल.

त्यांच्याकडे कमी संसाधने असल्याने, सोलो स्टेकर MEV संधींमधून नफा मिळवू शकणार नाहीत. यामुळे स्वतंत्र प्रमाणकांवर त्यांची कमाई वाढवण्यासाठी शक्तिशाली स्टेकिंग पूलमध्ये सामील होण्याचा दबाव वाढू शकतो, ज्यामुळे इथेरियममधील विकेंद्रीकरण कमी होईल.

परवानगीयुक्त मेमपूल

सँडविचिंग आणि फ्रंटरनिंग हल्ल्यांना प्रतिसाद म्हणून, व्यापारी व्यवहाराच्या गोपनीयतेसाठी प्रमाणकांसोबत साखळीबाह्य सौदे करण्यास सुरुवात करू शकतात. संभाव्य MEV व्यवहार सार्वजनिक मेमपूलमध्ये पाठवण्याऐवजी, व्यापारी तो थेट प्रमाणकाला पाठवतो, जो त्याचा ब्लॉकमध्ये समावेश करतो आणि व्यापाऱ्यासोबत नफा वाटून घेतो.

"डार्क पूल" ही या व्यवस्थेची एक मोठी आवृत्ती आहे आणि ती विशिष्ट शुल्क भरण्यास तयार असलेल्या वापरकर्त्यांसाठी खुली असलेली परवानगीयुक्त, केवळ-प्रवेश मेमपूल म्हणून कार्य करते. हा कल इथेरियमची परवानगीविना आणि विश्वासहीनता कमी करेल आणि संभाव्यतः ब्लॉकचेनला "पे-टू-प्ले" यंत्रणेत रूपांतरित करेल जी सर्वाधिक बोली लावणाऱ्याला अनुकूल असेल.

परवानगीयुक्त मेमपूल मागील विभागात वर्णन केलेल्या केंद्रीकरणाच्या धोक्यांना देखील गती देतील. एकाधिक प्रमाणक चालवणाऱ्या मोठ्या पूलांना व्यापारी आणि वापरकर्त्यांना व्यवहाराची गोपनीयता ऑफर केल्याने फायदा होण्याची शक्यता आहे, ज्यामुळे त्यांचा MEV महसूल वाढेल.

मर्ज-नंतरच्या इथेरियममध्ये या MEV-संबंधित समस्यांचा सामना करणे हे संशोधनाचे मुख्य क्षेत्र आहे. आजपर्यंत, द मर्ज नंतर इथेरियमच्या विकेंद्रीकरण आणि सुरक्षिततेवर MEV चा नकारात्मक प्रभाव कमी करण्यासाठी प्रस्तावित केलेले दोन उपाय म्हणजे प्रस्तावक-निर्माता विभाजन (PBS) आणि बिल्डर API (नवीन टॅबमध्ये उघडते).

प्रस्तावक-निर्माता विभाजन

प्रूफ-ऑफ-वर्क आणि प्रूफ-ऑफ-स्टेक या दोन्हीमध्ये, ब्लॉक तयार करणारा नोड एकमतामध्ये सहभागी होणाऱ्या इतर नोड्सना साखळीमध्ये जोडण्यासाठी प्रस्तावित करतो. दुसरा मायनर त्यावर तयार केल्यानंतर (PoW मध्ये) किंवा बहुसंख्य प्रमाणकांकडून (PoS मध्ये) त्याला प्रमाणीकरण मिळाल्यानंतर नवीन ब्लॉक कॅनोनिकल साखळीचा भाग बनतो.

ब्लॉक उत्पादक आणि ब्लॉक प्रस्तावक भूमिकांचे संयोजन हेच पूर्वी वर्णन केलेल्या बहुतेक MEV-संबंधित समस्या आणते. उदाहरणार्थ, MEV कमाई वाढवण्यासाठी टाइम-बँडिट हल्ल्यांमध्ये (नवीन टॅबमध्ये उघडते) साखळी पुनर्रचना ट्रिगर करण्यासाठी सहमती नोड्सना प्रोत्साहन दिले जाते.

प्रस्तावक-निर्माता विभाजन (PBS) (नवीन टॅबमध्ये उघडते) हे MEV चा प्रभाव कमी करण्यासाठी डिझाइन केले आहे, विशेषतः सहमती स्तरावर. PBS चे प्रमुख वैशिष्ट्य म्हणजे ब्लॉक उत्पादक आणि ब्लॉक प्रस्तावक नियमांचे पृथक्करण. प्रमाणक अजूनही ब्लॉक प्रस्तावित करण्यासाठी आणि त्यावर मत देण्यासाठी जबाबदार आहेत, परंतु ब्लॉक निर्माता नावाच्या विशेष संस्थांच्या नवीन वर्गाला व्यवहारांची क्रमवारी लावण्याचे आणि ब्लॉक तयार करण्याचे काम दिले जाते.

PBS अंतर्गत, ब्लॉक निर्माता एक व्यवहार बंडल तयार करतो आणि बीकन साखळी ब्लॉकमध्ये ("अंमलबजावणी पेलोड" म्हणून) त्याचा समावेश करण्यासाठी बोली लावतो. पुढील ब्लॉक प्रस्तावित करण्यासाठी निवडलेला प्रमाणक नंतर वेगवेगळ्या बोली तपासतो आणि सर्वाधिक फी असलेले बंडल निवडतो. PBS मूलत: एक लिलाव बाजार तयार करते, जिथे निर्माते ब्लॉकस्पेस विकणाऱ्या प्रमाणकांशी वाटाघाटी करतात.

सध्याचे PBS डिझाईन्स कमिट-रिव्हील स्कीम (नवीन टॅबमध्ये उघडते) वापरतात ज्यामध्ये निर्माते त्यांच्या बोलींसह ब्लॉकच्या सामग्रीसाठी (ब्लॉक हेडर) केवळ क्रिप्टोग्राफिक बांधिलकी प्रकाशित करतात. विजयी बोली स्वीकारल्यानंतर, प्रस्तावक एक स्वाक्षरी केलेला ब्लॉक प्रस्ताव तयार करतो ज्यामध्ये ब्लॉक हेडर समाविष्ट असतो. स्वाक्षरी केलेला ब्लॉक प्रस्ताव पाहिल्यानंतर ब्लॉक निर्मात्याने संपूर्ण ब्लॉक बॉडी प्रकाशित करणे अपेक्षित आहे आणि अंतिम झालेले होण्यापूर्वी त्याला प्रमाणकांकडून पुरेसे देखील मिळणे आवश्यक आहे.

प्रस्तावक-निर्माता विभाजन MEV चा प्रभाव कसा कमी करते?

इन-प्रोटोकॉल प्रस्तावक-निर्माता विभाजन प्रमाणकांच्या कक्षेतून MEV काढणे काढून टाकून एकमतावर MEV चा प्रभाव कमी करते. त्याऐवजी, विशेष हार्डवेअर चालवणारे ब्लॉक निर्माते पुढे जाऊन MEV संधी कॅप्चर करतील.

हे प्रमाणकांना MEV-संबंधित उत्पन्नापासून पूर्णपणे वगळत नाही, कारण निर्मात्यांना त्यांचे ब्लॉक प्रमाणकांद्वारे स्वीकारले जाण्यासाठी जास्त बोली लावावी लागते. तरीही, प्रमाणक आता MEV उत्पन्न ऑप्टिमाइझ करण्यावर थेट लक्ष केंद्रित करत नसल्यामुळे, टाइम-बँडिट हल्ल्यांचा धोका कमी होतो.

प्रस्तावक-निर्माता विभाजन MEV चे केंद्रीकरण धोके देखील कमी करते. उदाहरणार्थ, कमिट-रिव्हील स्कीमचा वापर केल्याने निर्मात्यांना प्रमाणकांवर विश्वास ठेवण्याची गरज दूर होते की ते MEV संधी चोरणार नाहीत किंवा इतर निर्मात्यांसमोर उघड करणार नाहीत. यामुळे सोलो स्टेकर्सना MEV चा लाभ मिळण्याचा अडथळा कमी होतो, अन्यथा, निर्माते साखळीबाह्य प्रतिष्ठा असलेल्या मोठ्या पूलांना पसंती देण्याकडे आणि त्यांच्यासोबत साखळीबाह्य सौदे करण्याकडे कल देतील.

त्याचप्रमाणे, प्रमाणकांना निर्मात्यांवर विश्वास ठेवण्याची गरज नाही की ते ब्लॉक बॉडी रोखून ठेवणार नाहीत किंवा अवैध ब्लॉक प्रकाशित करणार नाहीत कारण पेमेंट बिनशर्त आहे. प्रस्तावित ब्लॉक अनुपलब्ध असला किंवा इतर प्रमाणकांद्वारे अवैध घोषित केला तरीही प्रमाणकाची फी प्रक्रिया करते. नंतरच्या प्रकरणात, ब्लॉक फक्त टाकून दिला जातो, ज्यामुळे ब्लॉक निर्मात्याला सर्व व्यवहार शुल्क आणि MEV महसूल गमावावा लागतो.

बिल्डर API

प्रस्तावक-निर्माता विभाजन MEV काढण्याचे परिणाम कमी करण्याचे वचन देत असले तरी, त्याची अंमलबजावणी करण्यासाठी सहमती प्रोटोकॉलमध्ये बदल करणे आवश्यक आहे. विशेषतः, बीकन साखळी वरील फोर्क निवड नियम अद्यतनित करणे आवश्यक असेल. बिल्डर API (नवीन टॅबमध्ये उघडते) हा एक तात्पुरता उपाय आहे ज्याचा उद्देश प्रस्तावक-निर्माता विभाजनाची कार्यशील अंमलबजावणी प्रदान करणे आहे, जरी उच्च विश्वास गृहीतकांसह.

बिल्डर API ही इंजिन API (नवीन टॅबमध्ये उघडते) ची सुधारित आवृत्ती आहे जी सहमती स्तर क्लायंटद्वारे अंमलबजावणी स्तर क्लायंटकडून अंमलबजावणी पेलोडची विनंती करण्यासाठी वापरली जाते. प्रामाणिक प्रमाणक तपशीलामध्ये (नवीन टॅबमध्ये उघडते) वर्णन केल्याप्रमाणे, ब्लॉक प्रस्तावित करण्याच्या कर्तव्यांसाठी निवडलेले प्रमाणक कनेक्ट केलेल्या अंमलबजावणी क्लायंटकडून व्यवहार बंडलची विनंती करतात, ज्याचा ते प्रस्तावित बीकन साखळी ब्लॉकमध्ये समावेश करतात.

बिल्डर API प्रमाणक आणि अंमलबजावणी-स्तर क्लायंट यांच्यात मिडलवेअर म्हणून देखील कार्य करते; परंतु ते वेगळे आहे कारण ते बीकन साखळी वरील प्रमाणकांना बाह्य संस्थांकडून ब्लॉक मिळवण्याची परवानगी देते (अंमलबजावणी क्लायंट वापरून स्थानिक पातळीवर ब्लॉक तयार करण्याऐवजी).

बिल्डर API कसे कार्य करते याचे विहंगावलोकन खाली दिले आहे:

-

बिल्डर API प्रमाणकाला अंमलबजावणी स्तर क्लायंट चालवणाऱ्या ब्लॉक निर्मात्यांच्या नेटवर्कशी जोडते. PBS प्रमाणेच, निर्माते हे विशेष पक्ष आहेत जे संसाधन-केंद्रित ब्लॉक-बिल्डिंगमध्ये गुंतवणूक करतात आणि MEV + प्राधान्य टिप्समधून मिळणारा महसूल वाढवण्यासाठी वेगवेगळ्या धोरणांचा वापर करतात.

-

एक प्रमाणक (सहमती स्तर क्लायंट चालवणारा) निर्मात्यांच्या नेटवर्ककडून बोलींसह अंमलबजावणी पेलोडची विनंती करतो. निर्मात्यांच्या बोलींमध्ये अंमलबजावणी पेलोड हेडर—पेलोडच्या सामग्रीसाठी क्रिप्टोग्राफिक बांधिलकी—आणि प्रमाणकाला द्यायची फी असेल.

-

प्रमाणक येणाऱ्या बोलींचे पुनरावलोकन करतो आणि सर्वाधिक फी असलेला अंमलबजावणी पेलोड निवडतो. बिल्डर API वापरून, प्रमाणक एक "ब्लाइंडेड" बीकन ब्लॉक प्रस्ताव तयार करतो ज्यामध्ये फक्त त्यांची स्वाक्षरी आणि अंमलबजावणी पेलोड हेडर समाविष्ट असतो आणि तो निर्मात्याला पाठवतो.

-

बिल्डर API चालवणाऱ्या निर्मात्याने ब्लाइंडेड ब्लॉक प्रस्ताव पाहिल्यानंतर संपूर्ण अंमलबजावणी पेलोडसह प्रतिसाद देणे अपेक्षित आहे. हे प्रमाणकाला "स्वाक्षरी केलेला" बीकन ब्लॉक तयार करण्यास अनुमती देते, जो ते संपूर्ण नेटवर्कमध्ये प्रसारित करतात.

-

बिल्डर API वापरणाऱ्या प्रमाणकाने ब्लॉक निर्मात्याने त्वरित प्रतिसाद न दिल्यास स्थानिक पातळीवर ब्लॉक तयार करणे अपेक्षित आहे, जेणेकरून ते ब्लॉक प्रस्ताव बक्षीस गमावणार नाहीत. तथापि, प्रमाणक आता-उघड झालेले व्यवहार किंवा दुसरा संच वापरून दुसरा ब्लॉक तयार करू शकत नाही, कारण ते इक्विव्होकेशन (एकाच स्लॉटमध्ये दोन ब्लॉकवर स्वाक्षरी करणे) च्या बरोबरीचे असेल, जो एक स्लॅश करण्यायोग्य गुन्हा आहे.

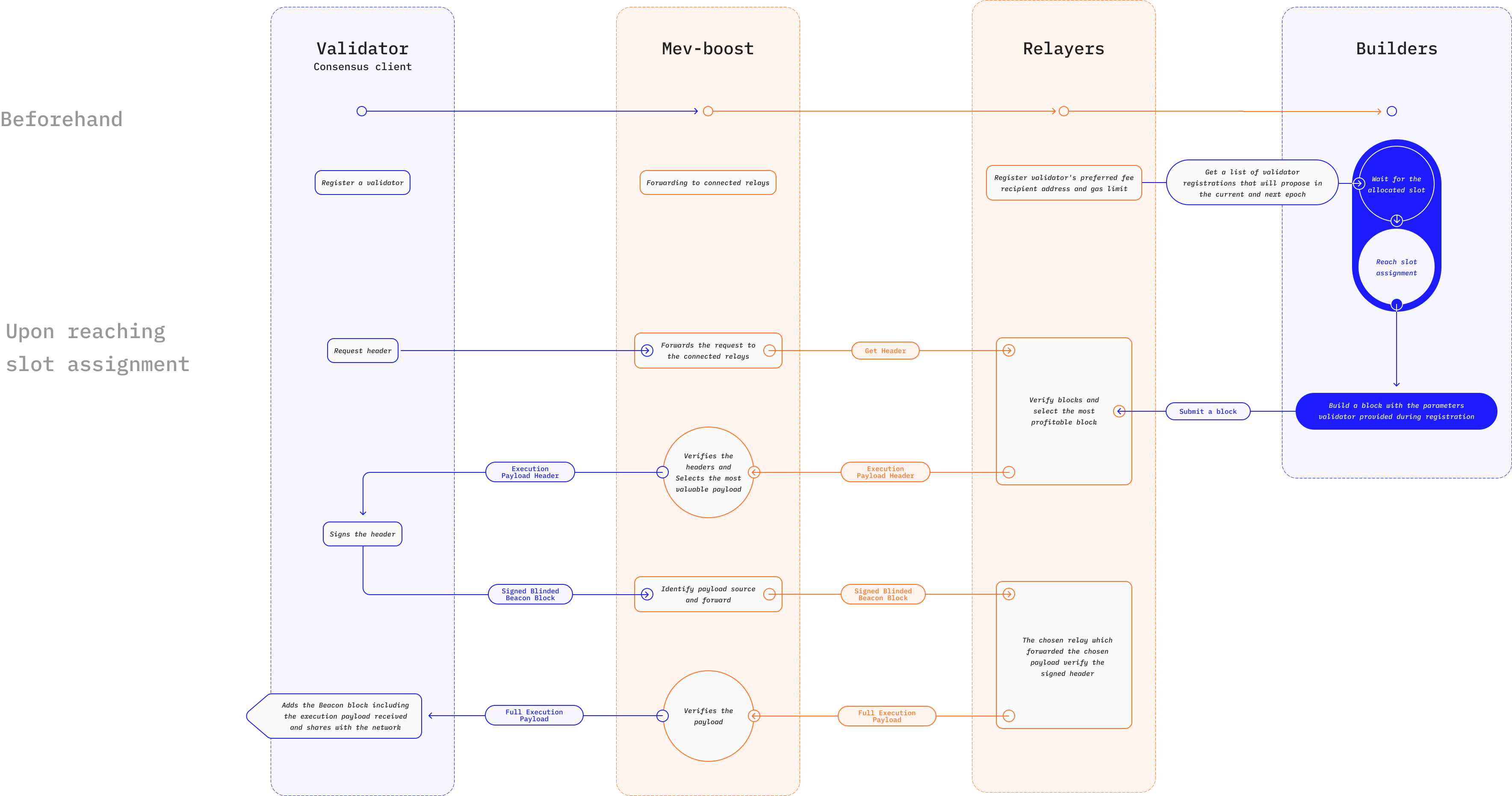

बिल्डर API चे एक उदाहरण अंमलबजावणी म्हणजे MEV-Boost (नवीन टॅबमध्ये उघडते), जी इथेरियमवरील MEV च्या नकारात्मक बाह्यतेवर आळा घालण्यासाठी डिझाइन केलेली Flashbots लिलाव यंत्रणेतील (नवीन टॅबमध्ये उघडते) सुधारणा आहे. Flashbots लिलाव प्रूफ-ऑफ-स्टेक मधील प्रमाणकांना फायदेशीर ब्लॉक तयार करण्याचे काम शोधक नावाच्या विशेष पक्षांना आउटसोर्स करण्याची परवानगी देतो.

शोधक फायदेशीर MEV संधी शोधतात आणि ब्लॉकमध्ये समावेश करण्यासाठी सीलबंद-किंमत बोलीसह (नवीन टॅबमध्ये उघडते) ब्लॉक प्रस्तावकांना व्यवहार बंडल पाठवतात. गो इथेरियम (गेथ) क्लायंटची फोर्क केलेली आवृत्ती mev-geth चालवणाऱ्या प्रमाणकाला फक्त सर्वाधिक नफा असलेले बंडल निवडायचे असते आणि नवीन ब्लॉकचा भाग म्हणून त्याचा समावेश करायचा असतो. ब्लॉक प्रस्तावकांचे (प्रमाणकांचे) स्पॅम आणि अवैध व्यवहारांपासून संरक्षण करण्यासाठी, व्यवहार बंडल प्रस्तावकापर्यंत पोहोचण्यापूर्वी प्रमाणीकरणासाठी रिलेअर्स मधून जातात.

MEV-Boost मूळ Flashbots लिलावाचे कार्य कायम ठेवते, जरी इथेरियमच्या प्रूफ-ऑफ-स्टेक मधील बदलासाठी डिझाइन केलेल्या नवीन वैशिष्ट्यांसह. शोधक अजूनही ब्लॉकमध्ये समावेश करण्यासाठी फायदेशीर MEV व्यवहार शोधतात, परंतु निर्माते नावाच्या विशेष पक्षांचा एक नवीन वर्ग व्यवहार आणि बंडल ब्लॉकमध्ये एकत्रित करण्यासाठी जबाबदार असतो. निर्माता शोधकांकडून सीलबंद-किंमत बोली स्वीकारतो आणि सर्वात फायदेशीर क्रमवारी शोधण्यासाठी ऑप्टिमायझेशन चालवतो.

रिलेअर अजूनही प्रस्तावकाकडे पाठवण्यापूर्वी व्यवहार बंडल प्रमाणित करण्यासाठी जबाबदार आहे. तथापि, MEV-Boost निर्मात्यांनी पाठवलेले ब्लॉक बॉडी आणि प्रमाणकांनी पाठवलेले ब्लॉक हेडर संचयित करून डेटा उपलब्धता प्रदान करण्यासाठी जबाबदार एस्क्रो सादर करते. येथे, रिलेशी जोडलेला प्रमाणक उपलब्ध अंमलबजावणी पेलोडची विनंती करतो आणि सर्वाधिक बोली + MEV टिप्ससह पेलोड हेडर निवडण्यासाठी MEV-Boost चे ऑर्डरिंग अल्गोरिदम वापरतो.

बिल्डर API MEV चा प्रभाव कसा कमी करते?

बिल्डर API चा मुख्य फायदा म्हणजे MEV संधींमध्ये प्रवेशाचे लोकशाहीकरण करण्याची त्याची क्षमता. कमिट-रिव्हील स्कीम वापरल्याने विश्वास गृहीतके दूर होतात आणि MEV चा लाभ घेऊ पाहणाऱ्या प्रमाणकांसाठी प्रवेशाचे अडथळे कमी होतात. यामुळे MEV नफा वाढवण्यासाठी मोठ्या स्टेकिंग पूलमध्ये समाकलित होण्यासाठी सोलो स्टेकर्सवरील दबाव कमी झाला पाहिजे.

बिल्डर API च्या व्यापक अंमलबजावणीमुळे ब्लॉक निर्मात्यांमध्ये अधिक स्पर्धेला प्रोत्साहन मिळेल, ज्यामुळे सेन्सॉरशिप प्रतिकार वाढतो. प्रमाणक एकाधिक निर्मात्यांच्या बोलींचे पुनरावलोकन करत असल्याने, एक किंवा अधिक वापरकर्ता व्यवहार सेन्सॉर करण्याचा हेतू असलेल्या निर्मात्याने यशस्वी होण्यासाठी इतर सर्व नॉन-सेन्सॉरिंग निर्मात्यांना मागे टाकले पाहिजे. यामुळे वापरकर्त्यांना सेन्सॉर करण्याचा खर्च नाटकीयरित्या वाढतो आणि या प्रथेला परावृत्त करतो.

काही प्रकल्प, जसे की MEV-Boost, फ्रंटरनिंग/सँडविचिंग हल्ले टाळण्याचा प्रयत्न करणाऱ्या व्यापाऱ्यांसारख्या विशिष्ट पक्षांना व्यवहाराची गोपनीयता प्रदान करण्यासाठी डिझाइन केलेल्या एकूण संरचनेचा भाग म्हणून बिल्डर API वापरतात. हे वापरकर्ते आणि ब्लॉक निर्माते यांच्यात खाजगी संप्रेषण चॅनेल प्रदान करून साध्य केले जाते. पूर्वी वर्णन केलेल्या परवानगीयुक्त मेमपूलच्या विपरीत, हा दृष्टिकोन खालील कारणांसाठी फायदेशीर आहे:

-

बाजारात एकाधिक निर्मात्यांचे अस्तित्व सेन्सॉरिंग अव्यवहार्य बनवते, ज्याचा वापरकर्त्यांना फायदा होतो. याउलट, केंद्रीकृत आणि विश्वासावर आधारित डार्क पूलचे अस्तित्व काही ब्लॉक निर्मात्यांच्या हातात सत्ता केंद्रित करेल आणि सेन्सॉरिंगची शक्यता वाढवेल.

-

बिल्डर API सॉफ्टवेअर ओपन-सोर्स आहे, जे कोणालाही ब्लॉक-निर्माता सेवा ऑफर करण्याची परवानगी देते. याचा अर्थ वापरकर्त्यांना कोणताही विशिष्ट ब्लॉक निर्माता वापरण्याची सक्ती केली जात नाही आणि इथेरियमची तटस्थता आणि परवानगीविना सुधारते. शिवाय, MEV-शोधणारे व्यापारी खाजगी व्यवहार चॅनेल वापरून अनवधानाने केंद्रीकरणास हातभार लावणार नाहीत.

संबंधित संसाधने

- Flashbots दस्तऐवज (नवीन टॅबमध्ये उघडते)

- Flashbots GitHub (नवीन टॅबमध्ये उघडते)

- mevboost.org (नवीन टॅबमध्ये उघडते) - MEV-Boost रिले आणि ब्लॉक निर्मात्यांसाठी रिअल-टाइम आकडेवारीसह ट्रॅकर

पुढील वाचन

- मायनर-काढण्यायोग्य मूल्य (MEV) म्हणजे काय? (नवीन टॅबमध्ये उघडते)

- MEV आणि मी (नवीन टॅबमध्ये उघडते)

- इथेरियम हे एक डार्क फॉरेस्ट आहे (नवीन टॅबमध्ये उघडते)

- डार्क फॉरेस्ट मधून सुटणे (नवीन टॅबमध्ये उघडते)

- Flashbots: MEV संकटाला फ्रंटरनिंग करणे (नवीन टॅबमध्ये उघडते)

- @bertcmiller चे MEV थ्रेड्स (नवीन टॅबमध्ये उघडते)

- MEV-Boost: मर्ज रेडी Flashbots आर्किटेक्चर (नवीन टॅबमध्ये उघडते)

- MEV-Boost म्हणजे काय (नवीन टॅबमध्ये उघडते)

- mev-boost का चालवावे? (नवीन टॅबमध्ये उघडते)

- द हिचहायकर्स गाईड टू इथेरियम (नवीन टॅबमध्ये उघडते)